ASC 842 Is Here to Stay: Lessons Learned from the Most Disruptive Lease Accounting Change in 40 Years

ASC 842 required companies to record operating leases as assets and liabilities on the balance sheet, ending the old practice of keeping them “off-balance-sheet.” Public companies spent millions transitioning to the standard, while private companies faced deadlines after December 15, 2021, with many rushing adoption through spreadsheets. This has created ongoing confusion and administrative challenges. The change improves financial transparency by showing long-term lease obligations that were previously hidden from investors and lenders.

For public companies, the transition to ASC 842 (Leases) was a multi-million-dollar project. For private companies, the deadlines have come and gone (fiscal years beginning after December 15, 2021 for most). Yet confusion persists. Many private companies adopted hastily, using spreadsheets, and are now realizing the ongoing burden.

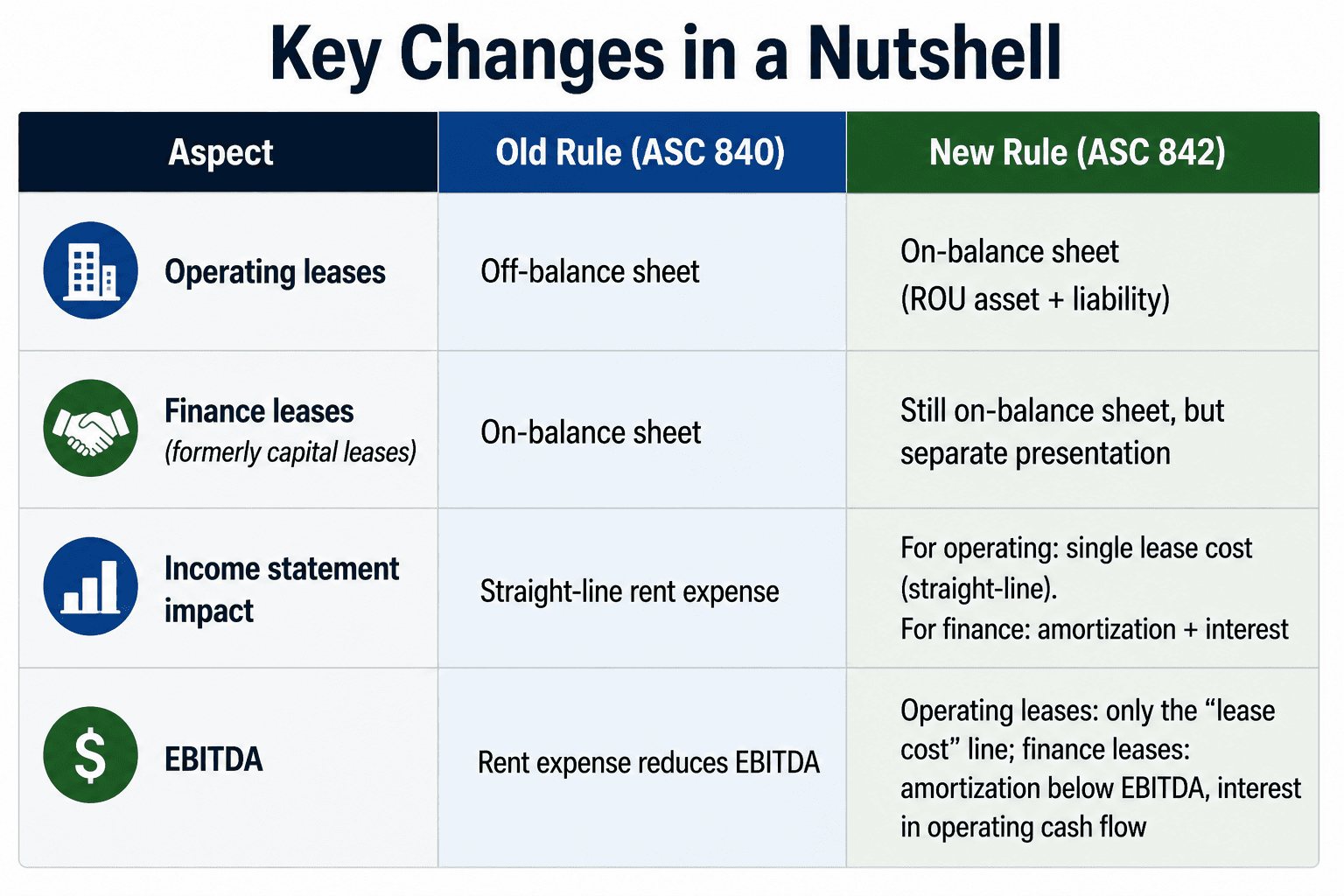

ASC 842 fundamentally changed how companies report leases. The core principle was simple but seismic: Operating leases now go on the balance sheet as assets and liabilities.

Prior to 842, operating leases were “off-balance-sheet financing.” A retailer could rent 500 stores, owe hundreds of millions in future rent, and show only the current month’s rent expense on the P&L. Investors and lenders could not see the long-term commitment.

Now, that same retailer must recognize:

- A Right-of-Use (ROU) asset (the value of the right to use the store)

- A Lease liability (the present value of remaining lease payments)

The Five Most Painful Lessons Learned in Year One

Lesson 1: Data Is King – And Excel Fails at Scale

To implement ASC 842, you need for every lease:

- Commencement date and term

- Renewal options (and probability of exercise)

- Payment schedule (including escalations, rent holidays, CAM charges)

- Discount rate (incremental borrowing rate or implicit rate)

Mid-sized companies with 50–200 leases discovered that this data was scattered across PDFs, email attachments, and physical filing cabinets. Spreadsheets become error-prone (e.g., incorrect calculation of present value due to off-by-one period errors). Lesson: Use lease accounting software like CoStar, LeaseQuery, or Nakisa. Even for 20 leases, the time savings and audit trail justify the cost.

Lesson 2: EBITDA Is Going Up – Impact on Debt Covenants

Under ASC 840, rent expense hit operating income, reducing EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). Under ASC 842 (operating leases), the straight-line lease cost is generally similar, but here’s the twist: Finance leases (which are more common after 842) split into amortization (below EBITDA) and interest (above operating cash flow but below EBITDA if you use the standard definition). This can inflate EBITDA.

Real-world impact: A company with a debt covenant requiring “EBITDA not less than $10M” might have been fine under 840 but saw EBITDA drop under 842. Or in some cases, increase. Lenders are amending credit agreements to add back certain lease expenses. Action item: Review your loan covenants and discuss with your lender if you haven’t already.

Lesson 3: Short-Term Leases – The “12-Month Exemption” Trap

ASC 842 provides a practical expedient: Leases with a term of 12 months or less (and no purchase option reasonably certain to exercise) do not need to be recognized on the balance sheet.

The trap: If you have a 12-month lease with a renewal option that you intend to exercise, the term is actually longer than 12 months. You are not exempt. This is a common audit finding. For example, a company signs a warehouse lease for 12 months, with an option to renew for another 12 months. Management says, “We’ll definitely renew.” Then the lease term is 24 months, and you must book the ROU asset and liability.

Lesson 4: Variable Lease Payments (CAM, Indexes) Are Tricky

Leases often require variable payments: common area maintenance (CAM), property taxes, insurance, or payments tied to an index (e.g., CPI). Under ASC 842, you include in the liability only those variable payments that are based on an index or rate (and use the starting index). You do not include CAM or usage-based payments (like rent based on a percentage of sales) unless they are in-substance fixed

Common error: Companies either include all variable payments (overstating liability) or none (understating). The correct approach requires careful reading of each lease contract.

Lesson 5: Transition and Modified Retrospective Approach Was Confusing

Most private companies used the “modified retrospective” method, which means they did not restate prior periods. They simply recognized a cumulative-effect adjustment to retained earnings as of the beginning of the earliest period presented.

But that created comparability issues. A lender looking at 2021 (pre-842) vs. 2022 (post-842) sees different balance sheet totals. Best practice: Provide a clear footnote explaining the impact of adoption and, if useful, a supplemental schedule showing what the prior year would have looked like under 842.

Practical Implementation Checklist (For Those Still Struggling)

If you adopted with spreadsheets and are now facing audit difficulties, here is a rescue plan:

- Inventory all leases – Real estate, vehicles, copiers, IT equipment. Don’t forget embedded leases (e.g., a contract to use a specific shipping container).

- Extract key terms – Use a standardized template. For each lease, note the commencement, term, renewal options, termination penalties, and payment schedule.

- Determine discount rate – For operating leases where the implicit rate is unknown (most cases), use your incremental borrowing rate (IBR). For private companies, this is often the rate a bank would charge for a secured loan of similar term. You can use a risk-free rate plus a credit spread.

- Calculate present value – Use the NPV function in Excel (being careful with timing: payments at beginning vs. end of period). Or use software.

- Record the journal entry – Debit ROU asset, Credit Lease liability (for present value of remaining payments). Adjust for initial direct costs and prepaid rent.

- Set up amortization schedule – For operating leases: the ROU asset amortizes (usually straight-line) and the liability reduces as payments are made. For finance leases: separate interest and principal.

- Disclose – Include qualitative and quantitative disclosures: maturity analysis of lease liabilities, weighted-average discount rate, weighted-average remaining term.

“ASC 842 is not a fad. It is now a permanent feature of US GAAP. If your adoption was rushed, schedule a post-implementation review. Clean up your lease data, reconsider software if your lease count exceeds 20, and communicate with lenders about covenant calculations. The firms that embrace the spirit of 842 (transparency) will benefit from better internal decision-making about whether to lease or buy.”

Tags:

Found this helpful? Share it with your network.