Cash Flow vs. Profit: Why Your P&L Can Be Green While Your Bank Account Is Red

It’s the most confusing paradox in business: “We just had our best quarter ever—record sales, record gross margin. So why can’t I make payroll?” This question haunts owners of growing companies, especially in retail, construction, manufacturing, and professional services. The answer lies in the difference between accrual accounting (which gives you profit) and liquidity (which gives you cash). Understanding this distinction is not academic. According to a U.S. Bank study, 82% of business failures are caused by poor cash flow management, not lack of profit.

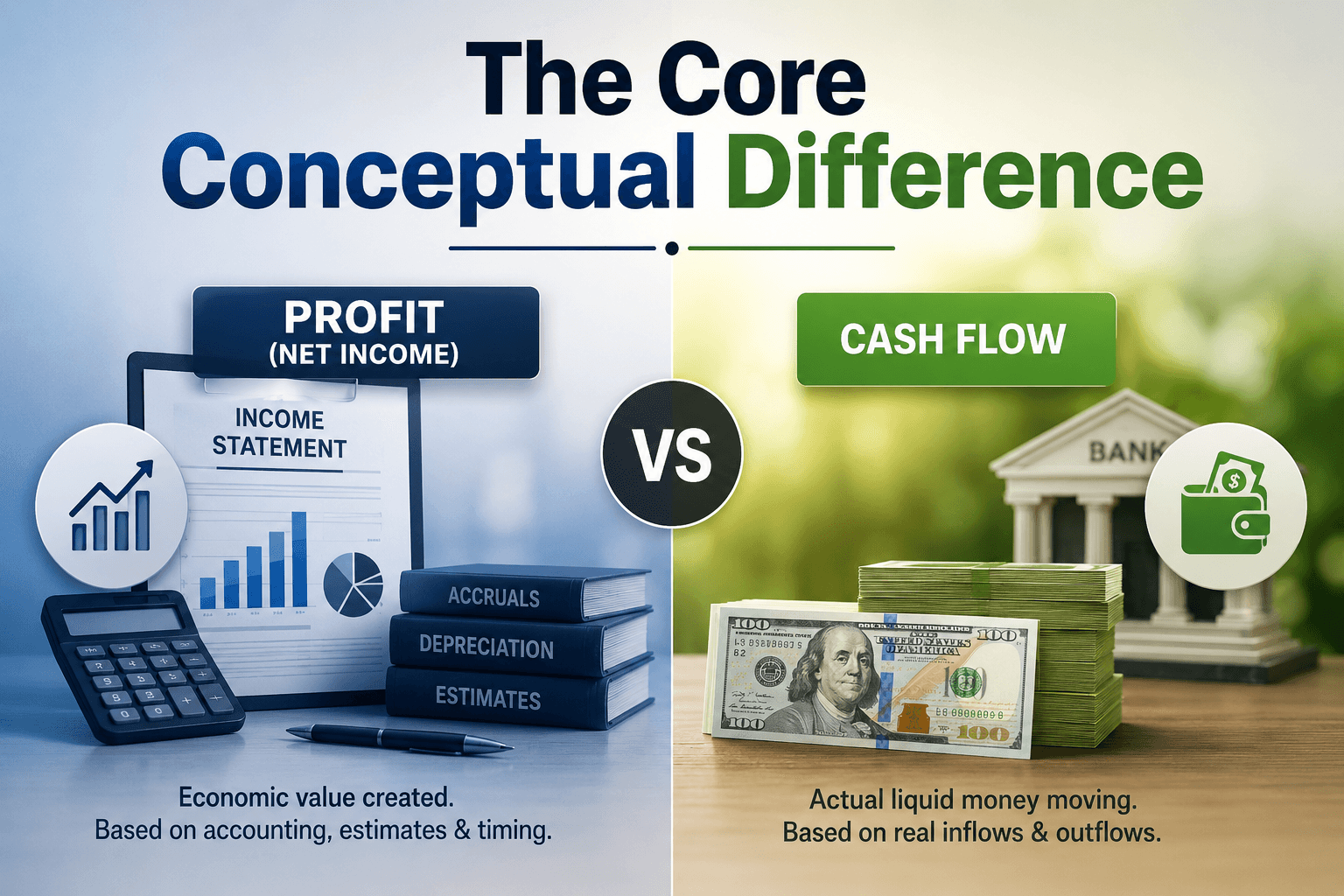

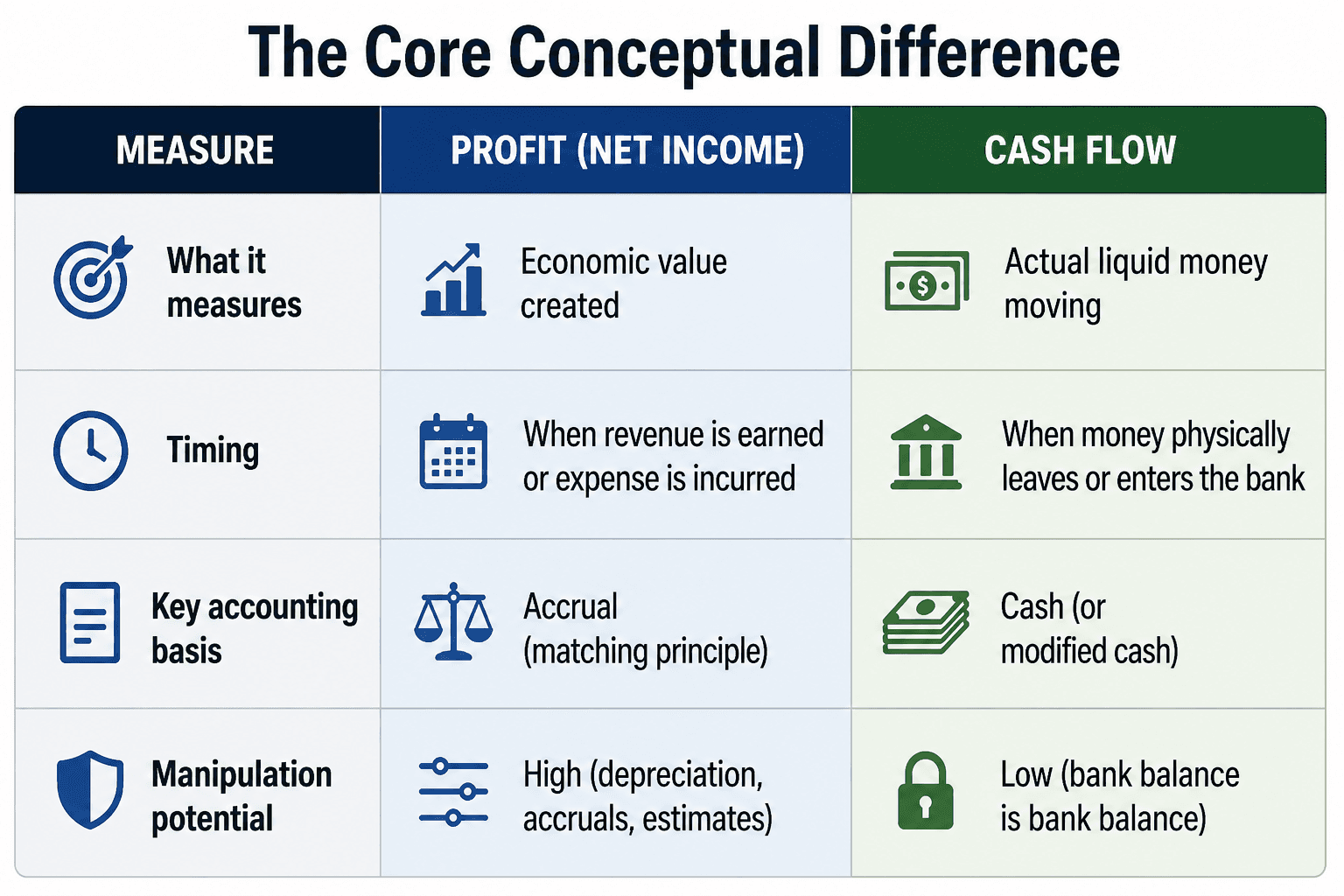

The Core Conceptual Difference

Let’s walk through a concrete example.

Case Study: The Profitable but Bankrupt Landscaper

Company: GreenCut Landscaping (annual revenue $2M)

March 15: Signs a $100,000 contract to design and install a corporate campus garden. Work will be done in April.

April: GreenCut buys 40 , 000 o f p l a n t s , m u l c h , a n d s t o n e ( p a i d c a s h ) . I t p a y s 40,000ofplants,mulch,andstone(paidcash).Itpays30,000 in labor (cash). It finishes the job.

May 1: GreenCut sends an invoice for $100,000 with “Net 60” terms (customer has 60 days to pay).

Accrual Accounting (April P&L):

- Revenue: $100,000 (earned because work is complete)

- COGS: $70,000 (plants + labor)

- Gross profit: $30,000 (looks good!)

Cash Reality (April bank account):

- Opening balance: $20,000

- Outflows: $70,000 (plants + labor)

- Inflows: $0

- Ending balance: -$50,000 (overdraft)

GreenCut is profitable on paper but technically insolvent. It cannot pay rent on May 1 or buy fuel for its trucks.

The Danger Zone: Overtrading

Overtrading (also called “over-trading”) occurs when a business grows its sales faster than it can fund the associated working capital. It is the silent killer of high-growth SMEs.

How overtrading kills:

- You win a huge order from a big customer (exciting!).

- To fulfill it, you must pay suppliers and staff today.

- The customer pays in 60–90 days (standard for large corporates).

- You run out of cash to finance the gap. You delay paying suppliers; they cut you off. You miss payroll; good employees leave. You become a casualty of your own success.

Early warning signs of overtrading:

- Revenue growing >25% year-over-year but cash balance shrinking.

- Days Sales Outstanding (DSO) increasing (customers taking longer to pay).

- Days Payable Outstanding (DPO) decreasing (you paying faster, maybe because suppliers are demanding cash on delivery).

- Inventory turnover increasing too quickly (you can’t stock enough to meet demand).

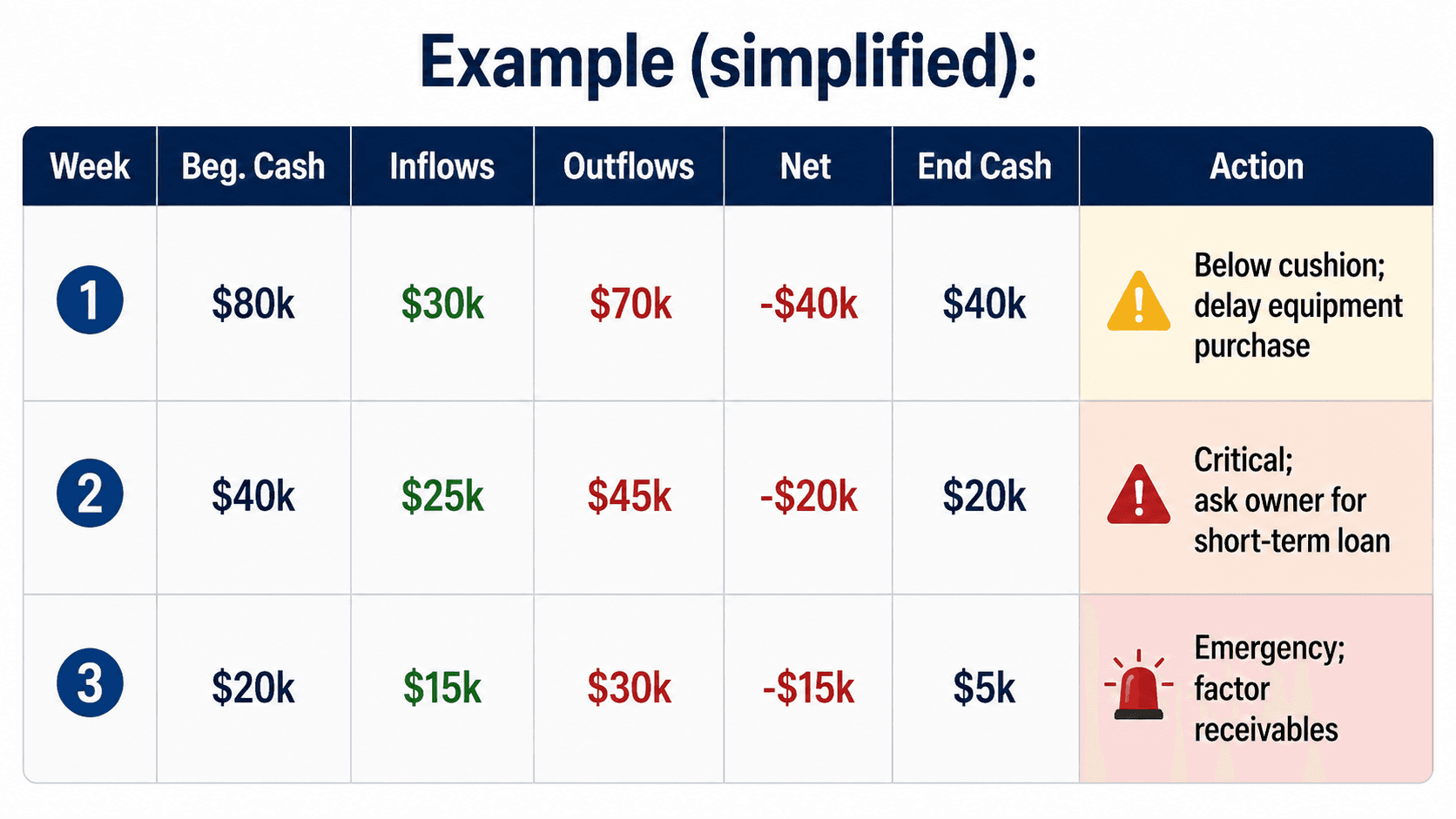

The Solution: Run a 13-Week Cash Flow Forecast

A P&L tells you what happened in the past. A cash flow forecast tells you if you’ll be alive next Tuesday. Every business with less than $50M in revenue should maintain a rolling 13-week cash flow forecast.

How to build one (in Excel or a tool like Float, CashAnalytic, or Centage):

Step 1: List all cash inflows by week

- Customer collections (based on your payment terms, not your invoices)

- Owner capital contributions

- Loan proceeds

- Tax refunds

Step 2: List all cash outflows by week

- Payroll (gross + taxes + benefits)

- Rent, utilities, insurance

- Supplier payments (based on when you actually pay, not the invoice date)

- Debt service (principal + interest)

- Debt service (principal + interest)

- Estimated tax payments

Step 3: Calculate net cash flow per week (Inflows – Outflows)

Step 4: Add beginning cash balance to get ending balance

Step 5: Flag any week where ending balance goes below your minimum required cushion (e.g., $50,000).

Practical Tactics to Improve Cash Flow

1. Negotiate better terms with vendors.

If you pay suppliers in 30 days but your customers pay you in 60, you are financing your customers. Ask vendors for Net-60. Offer to pay early in exchange for a 2% discount (2/10 net 30).

2. Get deposits from customers.

For any job over $10,000, ask for 30-50% upfront. For custom work, 100% upfront. This is standard in many industries (web design, construction, consulting).

3. Use a line of credit BEFORE you need it.

Banks won’t lend to you when you’re overdrawn. Set up a revolving line of credit when cash is healthy. Use it only to bridge timing gaps (e.g., draw $50k on May 15, repay on June 30 when customer pays).

4. Speed up invoicing and collections.

Invoice the same day you deliver the product or service. Automate payment reminders (day 1, day 15, day 30 past due). Offer credit card payments (yes, the fee is worth avoiding a cash crisis).

5. Factor your receivables (last resort).

Sell your unpaid invoices to a factoring company at a discount (e.g., 95 cents on the dollar). Expensive, but it can save you from bankruptcy.

“Profit is an opinion based on accounting rules. Cash is a fact based on bank statements. You can eat profit on paper, but you pay employees and suppliers with cash. Prioritize a rolling 13-week forecast, negotiate payment terms aggressively, and never confuse a profitable quarter with a liquid company.”

Tags:

Found this helpful? Share it with your network.