FP&A vs. Traditional Accounting: Building a Bridge Between Historical Accuracy and Future Agility

Finance departments often experience tension between accounting and FP&A teams. Accounting focuses on accuracy, compliance, and detailed financial records, while FP&A prioritizes forecasting, flexibility, and quick decision-making. In small companies, one person may handle both roles, while larger organizations often separate them, creating conflicts that can lead to budgeting issues and frustration. However, this divide can be overcome by recognizing their different priorities and fostering collaboration, allowing both functions to support strategic growth and financial stability together.

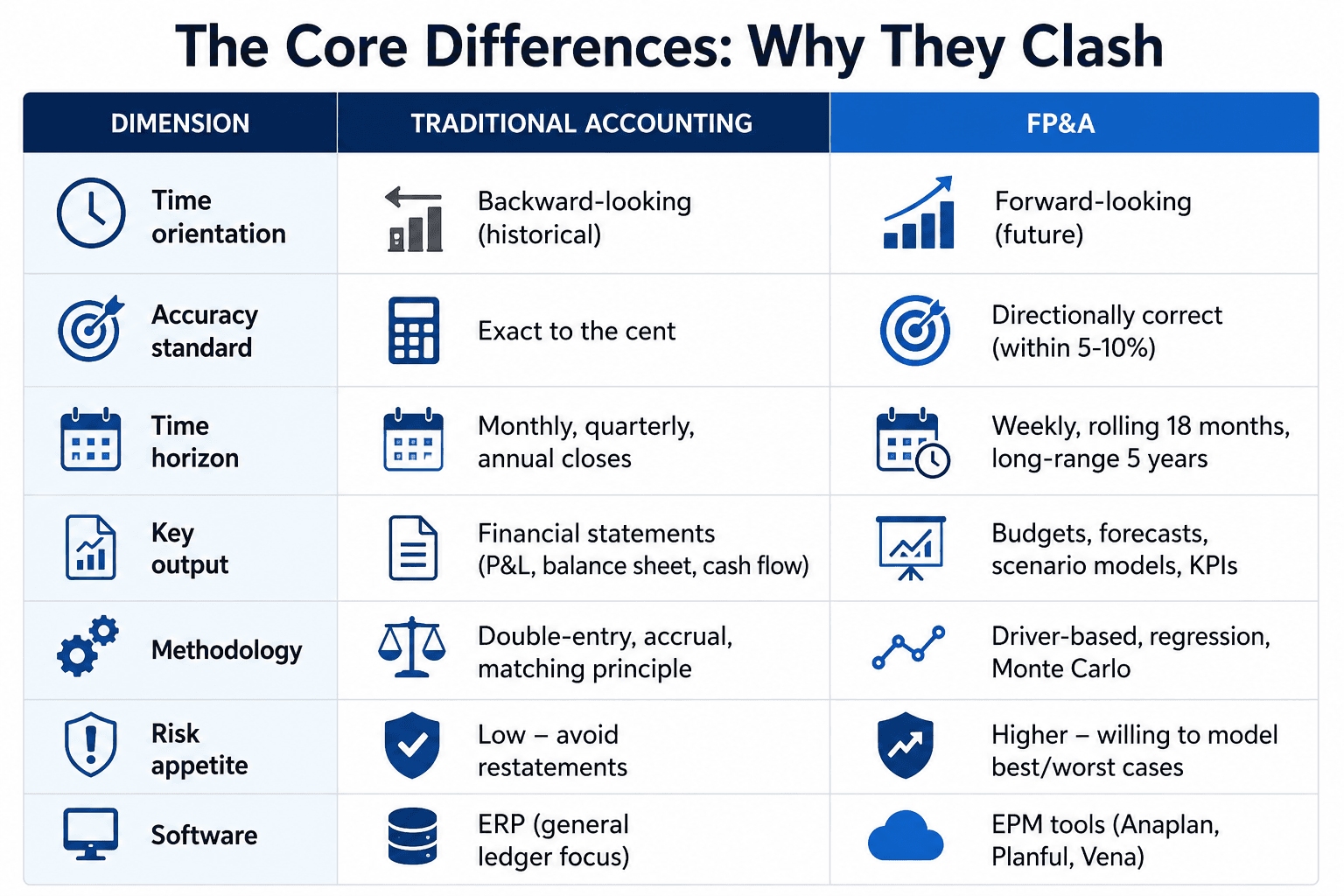

There is a quiet war in many finance departments. On one side sits the Controller or Chief Accounting Officer, whose world is built on GAAP, audit trails, and precision to the penny. On the other side sits the FP&A Director (Financial Planning & Analysis), who deals with rolling forecasts, driver-based models, and “good enough” speed.

In small companies, this conflict is internalized by one person trying to wear both hats. In larger ones, it becomes a structural divide. The result? Missed budgets, frustrated analysts, and a CFO caught in the middle.

But the tension is not inevitable. By understanding the fundamental differences and intentionally building bridges, you can turn FP&A and accounting into a symbiotic relationship—one that drives strategic growth while maintaining financial integrity.

The Conflict Expressed in Everyday Scenarios

Scenario A: The Monthly Close Delay

The accounting team needs 10 days to close the books because they meticulously check every reconciliation. FP&A needs final numbers on day 3 to issue the quarterly forecast to the board. Accounting says, “You can’t forecast until I’m sure.” FP&A says, “Then we’ll miss the board deadline.” Result: FP&A uses estimates that later differ from actuals, eroding trust.

Scenario B: The Variance Explanation

Accounting reports that SG&A expenses are $50,000 over budget. FP&A built the budget based on driver-based assumptions (headcount + marketing spend). But accounting accrued an unexpected legal fee. Instead of collaborating to explain, accounting sends a terse variance report, and FP&A gets blamed for “unrealistic budget.”

Scenario C: The New Product Launch

FP&A wants to model a new product’s profitability using contribution margin. Accounting insists on fully allocated overhead (including rent, IT, etc.). The model then shows the product losing money, so the launch is canceled. Later, a competitor launches the same product and succeeds, because their accounting team separated incremental vs. sunk costs.

How to Bridge the Divide: 4 Concrete Strategies

Strategy 1: Create a Single Source of Truth (The Data Layer)

Most fights start because FP&A is working from a different dataset than accounting. FP&A exports the trial balance, manipulates it in Excel, and loses the link to the GL. Accounting changes a journal entry after the export. Chaos ensues.

Solution: Implement a data warehouse or an EPM tool that connects directly to the ERP. FP&A should never touch the raw GL. Instead, they access a curated, read-only “reporting layer” that is updated daily with closed-period data. Accounting controls the source; FP&A consumes the output.

Tool examples: For small companies, Fathom or Spotlight Reporting. For mid-market, Vena or Planful. For enterprise, Anaplan or SAP Analytics Cloud.

Strategy 2: Establish a “Close-to-Forecast” Handoff Protocol

Define a formal cadence:

- Day M+2 (2 days after month-end): Accounting provides “flash numbers” – preliminary actuals with 95% confidence. FP&A uses these for a preliminary forecast update.

- Day M+7: Accounting provides final, audited actuals.

- Day M+8-10: FP&A reconciles the forecast to final actuals, notes variances >5%, and sends a variance commentary to accounting for review.

- Day M+11: FP&A issues the official rolling forecast.

Key document: A Forecast Assumption Log that records every estimate used (e.g., “Accrued bonus assumed 50% of target, awaiting HR confirmation”). When final numbers come in, the log explains the delta.

Strategy 3: Rotate Your Talent (The Empathy Strategy)

The best finance organizations force cross-pollination. Consider these rotations:

- GL Accountants spend 2 months in FP&A – They learn that not every number needs to be perfect to be useful. They see how their month-end timing delays strategic decisions.

- FP&A Analysts spend 2 months in Accounting – They learn the pain of reconciling intercompany transactions and why a seemingly simple adjustment might break a control. They gain respect for compliance.

Even a “shadowing week” once a quarter can reduce friction. As one CFO told me: “My FP&A director used to complain about slow closes. After she spent a week watching bank reconciliations, she never complained again – and she even helped automate the process.”

Strategy 4: Redefine the Performance Review

Most performance metrics for accounting emphasize accuracy and deadlines (e.g., “Close within 7 days, 0 restatements”). For FP&A, the metrics emphasize forecast accuracy (e.g., “Revenue forecast within 5% of actual, 8 quarters out”) and business impact (e.g., “Model guided pricing decision that increased margin by 200 bps”).

The bridge metric: Create a shared KPI – Time from close to forecast publication. This forces both teams to collaborate. Accounting wins when they close faster (without sacrificing quality). FP&A wins when they publish sooner. Everyone wins when the number is low.

What a Healthy FP&A-Accounting Relationship Looks Like

- Monthly “pre-close” meeting: Accounting shares known adjusting entries (accruals, reclasses) that will hit the GL. FP&A shares any variances they are seeing from their operational data (e.g., salesforce bookings).

- Joint review of material variances: Anything >10% or >$100k gets a joint explanation signed off by both leads.

- Shared budget ownership: Accounting helps validate the budget’s historical rationale (e.g., “Last year’s rent was $120k, your 5% increase is reasonable”). FP&A builds the future assumptions.

- Mutual respect: Accounting stops calling FP&A “voodoo forecasters.” FP&A stops calling accounting “historians.”

“Accuracy without agility leads to irrelevance – you produce perfectly correct numbers that help no one make decisions. Agility without accuracy leads to chaos – you move fast but fly blind. The modern finance function needs both. Build the bridge between FP&A and traditional accounting through data governance, clear handoffs, talent rotation, and shared metrics. The result is a finance department that is both trusted and strategic.”

Tags:

Found this helpful? Share it with your network.